What scammers do the week your spouse dies

- A death certificate can start a chain of public records and data updates that scammers may exploit.

- Data brokers may expose details about your household, property, relatives and recent loss.

- Fake debt collectors, insurance agents and government callers may target grieving spouses within days.

- Freezing credit and verifying every payment request can help reduce the risk fast.

You don’t have to publish an obituary for this to happen to you. That’s the first thing most people get wrong. They think the risk comes from the tribute they write, the details they share online or the words they choose for the service announcement.

The risk starts before any of that. It starts the moment a death certificate gets filed. A death certificate does more than document a death. It can act like a signal that moves through government databases, county records, property filings and data broker pipelines automatically, relentlessly and, in many states, publicly.

By the time you’re home from the funeral, that signal may have already reached people waiting for it. Here’s exactly what that looks like, phase by phase, and what you can do to disrupt it before scammers use it against you.

Phase 1 (Day 1-3): The paperwork you can’t avoid starts moving

When someone dies, the funeral home files a death certificate with the state’s vital records office. This isn’t optional. It’s required before cremation can proceed, before benefits can be claimed, before anything else can happen. What most people don’t realize is where that record goes next and how quickly.

State death records vary in accessibility. Some states treat them as fully public, nearly immediately. Michigan, Minnesota, North Carolina, Massachusetts, and Montana are among the states where death records are accessible to virtually anyone who requests them. Other states restrict access to immediate family for a period of years, but even restricted records flow to entities that qualify as “interested parties,” a category that includes insurance companies, financial institutions, and in many cases, commercial data brokers.

The funeral home also reports the death to the Social Security Administration, typically within days. That triggers the Death Master File update, a federal database that certified entities, including many data aggregators, receive on a weekly basis.

And then there’s the obituary. Not everyone publishes one. But for those who do: cybersecurity researchers have documented that automated scrapers monitor obituary pages continuously, beginning within hours of publication. AI tools extract names, relationships, cities, ages, military service, church affiliation, employment history, everything. The obituary doesn’t create the exposure. It massively accelerates it.

By the end of Day 3, a data broker profile that already existed on you has been quietly refreshed. It now carries a new status signal: recently bereaved. That status alone changes everything about how you’re targeted.

Phase 2 (Days 4-14): Your profile gets upgraded. You don’t know it’s happening.

Data broker profiles do more than list your contact information. Companies like Spokeo, Whitepages, BeenVerified and others may collect details about your household, property, estimated income and relatives. After a spouse dies, that profile can change fast. To criminals, those changes can become extremely valuable. In fact, scammers are not always guessing. They often build targeting lists.

Public records and commercial data can point to terms like “recently widowed” or “newly single homeowner.” As a result, a scammer may learn a lot about your life right now. For example, you could be managing money alone for the first time. You could also be dealing with an inheritance. At the same time, grief, paperwork and urgent decisions may be consuming your attention. That is exactly the kind of moment scammers try to exploit.

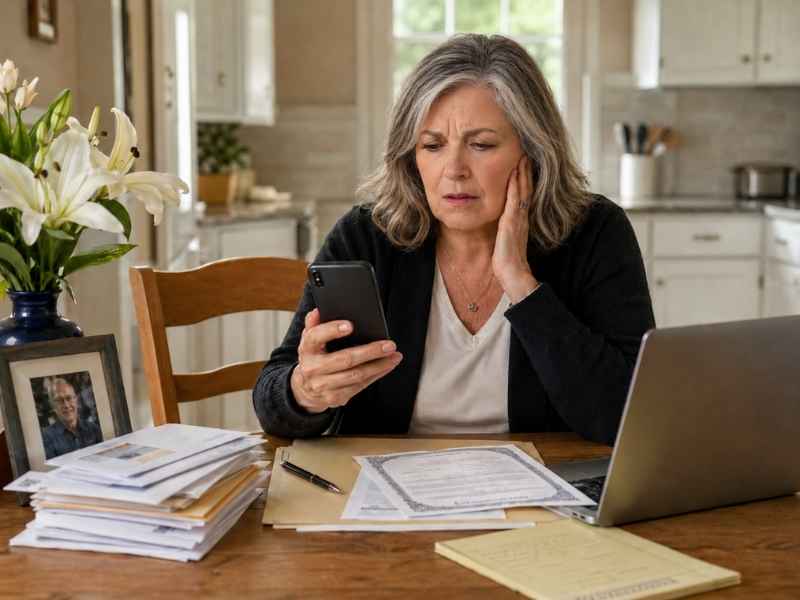

Within the first two weeks, the calls may begin. They can sound official and confident. The caller may know your spouse’s name. They might also mention where your spouse worked or share a detail that feels too specific to be random. That detail may have come from your data broker profile. It could also come from an obituary, death record or social media post. Either way, the scripts may change, but the goal is usually the same:

The fake debt collector

“I’m calling about an outstanding balance on your spouse’s account.” The chaos and confusion that follow a death can give fraudsters the perfect opening. They may pretend to be debt collectors, government agents or life insurance agents. Their goal is to make the surviving spouse panic and pay fast.

Any caller demanding immediate personal payment should raise a red flag. That is especially true if they ask for a wire transfer, gift card, payment app or cryptocurrency. Do not pay on the spot. Ask for the caller’s name, company and callback number. Then hang up and contact the real company, agency or your estate attorney directly. Any real debt collector must provide written debt validation. A scammer will usually pressure you to act before you can verify anything.

The fake insurance agent

“There’s an unclaimed policy in your spouse’s name. We just need to verify a few details.” The goal isn’t to pay you anything. It’s to extract your Social Security number, account numbers, or security question answers under the guise of processing a claim.

The fake government official

“We need to confirm your spouse’s Social Security number to release the final benefit.” The SSA does not call you unsolicited to ask for this. Neither does Medicare. Neither does the IRS.

If you receive any of these calls, ask for the caller’s name, the organization and a callback number. Then hang up and contact the actual institution directly using a phone number from its official website, app or a trusted source. Never use a number a caller gives you.

Phase 3 (Weeks 2-8): The paperwork you file becomes a public map

Here’s the part no one talks about. If you need to transfer the home into your name alone, you may have to file paperwork at the county recorder’s office. Depending on how the property was held, this is either an affidavit of survivorship, a new deed, or documentation from the probate court. The specific form varies by state.

What doesn’t vary much: property records are generally public, although access rules and online availability vary by location. The county recorder’s office is one of the primary data sources that data brokers ingest. The moment that the deed transfer is recorded, your data broker profile updates again. Now it reflects something new: you are the sole owner of a property that was previously held jointly. Your household composition just changed from two to one. That’s a financial signal. And it reaches people who are specifically watching for it.

Around the same time, if the estate requires probate, that filing becomes public, too. In most jurisdictions, probate records are accessible to anyone, and they can reveal the value of the estate, a list of assets, the names of beneficiaries, and the executor’s identity. Predatory calls and letters that begin just weeks after filing probate paperwork are not coincidental.

Fraudsters pose as attorneys, debt collectors, and estate service providers, each demanding immediate payment of invented fees. This is sometimes called the “inheritance trap,” and it’s a growing category of fraud that begins the moment the filing appears in the public record. If you have an estate attorney, lean on them hard during this window. Any unsolicited contact about the estate, by phone, mail, or email, should be verified directly with your attorney before any response.

Phase 4 (Weeks 3-12): The ghosting window

While you’re managing the estate, someone may already be applying for credit in your spouse’s name. It’s called ghosting, a form of identity theft where criminals use the personal information of someone who has died. The risk is real because families may not discover the fraud until bills, statements or collection notices arrive later. The window of vulnerability exists because of a timing gap most families never anticipate: financial institutions, credit bureaus, and the IRS can take from weeks to months to fully register and share death records across their systems. Criminals know this gap exists. They exploit it deliberately.

Using information harvested from the obituary, the death record, or a dark web purchase of the deceased’s Social Security number, a ghoster can open credit cards, apply for loans, file a fraudulent tax return to claim a refund, or access health benefits, all in your spouse’s name, before any institution has flagged the account as deceased. You likely won’t know this is happening. The statements go to your address. But they often arrive months later, after the damage is done and the trail has gone cold.

The fix is straightforward but time-sensitive: freeze your spouse’s credit at all three bureaus, Equifax, TransUnion, and Experian, as soon as you have a death certificate in hand. Provide a copy of the death certificate to each bureau. This closes the window. Pull their credit report now, too, before you freeze it, to check for anything already opened fraudulently.

Phase 5 (Weeks 4 and beyond): The long game

Not every scammer wants a quick payment. Some of the most financially devastating attacks take weeks to build, because the goal isn’t a transaction, it’s a relationship. By the fourth week, obituary data, death records, property filings, and data broker profiles have combined into something that gives a skilled criminal real leverage. They know your name, your address, your approximate financial picture, your adult children’s names and cities, your spouse’s career, and exactly what just happened in your life.

That last part is the key. The scam doesn’t start with a lie. It starts with something true. Obit-scouring criminals pretend to be long-lost friends or relatives of the deceased, contacting surviving spouses out of the blue to commiserate and reminisce. These displays of simulated compassion can evolve into romance scams or attempts to defraud beneficiaries out of inheritance money.

They mention something specific, such as a place your spouse worked, a neighborhood they grew up in or a detail that feels too accurate to come from a stranger. That detail came from a public record.

The FBI says people over 60 reported more than $7.7 billion in fraud losses in 2025. Confidence and romance scams remain especially dangerous because they can build slowly over time. And the average loss per victim reached $38,500. The scammer’s advantage is cruel in its simplicity: they already know what just happened in your life. That makes their reaching out feel personal, familiar, and safe.

The underlying problem and why one action doesn’t fix it

Here’s what connects every phase of this timeline: the data broker ecosystem. The obituary, the death record, the property deed transfer, the probate filing, none of these individually would be as dangerous without the broker infrastructure that aggregates them, cross-references them, and makes them searchable in a single profile by anyone willing to pay a few dollars.

Your data broker profile existed before your spouse died. Their death just supercharged it. And once your updated profile is out there, it circulates. It gets bought, sold, and refreshed. Removing it once isn’t enough; data brokers re-list information constantly as they ingest new sources. This is the problem Incogni was built to address. Rather than spending hours manually submitting opt-out requests to hundreds of individual brokers, each with its own form, its own timeline, and its own tendency to re-list you, Incogni automates the process. It contacts 420+ data brokers on your behalf, requests removal, and keeps monitoring those sites when your data reappears. Because it will.

Exclusive Deal for CyberGuy Readers (60% off): Incogni offers a 30-day, money-back guarantee and applies a special CyberGuy discount to all annual plans, as low as $6.39/month for one person (billed annually) or $13.19/month for your family (up to 5 people). This fully automated data removal service provides ongoing protection from 420+ data brokers, and the Unlimited plan allows you to request removals from specific sites where your personal information appears.

I recommend the family plan. It works out to only $2.64 per person per month (or $4.80 per person per month for the Family Unlimited plan) for powerful, year-round privacy protection. It’s an excellent service, and well worth trying to see exactly how much of your information is being exposed right now.

Get Incogni and remove your info

The four things to do in the first two weeks

You’re managing enough. Keep this short list somewhere you can find it.

1) Freeze the credit. For both of you

Freeze your deceased spouse’s credit with Equifax, TransUnion, and Experian using a death certificate. Then freeze your own credit, too. Your profile is newly attractive to scammers. This is the single most time-sensitive action on this list.

2) Pull their credit report before you freeze it

Check for accounts you don’t recognize. Ghosting can begin within days of a death. The sooner you spot it, the easier it is to dispute.

3) Verify before you pay anything

Any call or letter claiming your spouse owed money, especially if they want a wire transfer or gift card payment, should be treated as a scam until proven otherwise. Ask for written debt validation. Debt collectors generally must provide written validation information within five days of first contacting you, unless they already included it in the first message.

4) Start removing your data from broker sites

Search your own name on Spokeo, Whitepages, or BeenVerified and see what’s already there. Then let a service like Incogni handle the ongoing removal. This isn’t a one-time task; it’s a continuous process, which is why automation matters.

5) Run a free exposure scan

You can also run a free exposure scan to see where your personal information is appearing online. Results typically arrive by email within an hour.

Related Links:

- Remove your data to protect your retirement from scammers

- Why widows and divorced women are targets for retirement scams

- Scams that aren’t illegal (but should be)

Kurt’s key takeaways

Bereavement fraud is cruel because it targets families at their weakest moment. The risk can begin as soon as a death certificate is filed. From there, public records, probate filings and data brokers can expose details scammers use fast. That is why every unexpected call about money should be verified. Do not trust a caller just because they know a name, address or family detail. Hang up and contact the real company, agency or estate attorney yourself. Also, freeze your loved one’s credit as soon as you have the death certificate. Then freeze your own credit, too. Scammers look for grieving spouses, newly single homeowners and families dealing with estate paperwork. You are not powerless. Act early, verify everything and remove your personal information from data broker sites before scammers use it against you.

Should death records and probate filings still be so easy for strangers and data brokers to access when grieving families are the ones paying the price? Let us know in the comments below.

FOR MORE OF MY TECH TIPS & SECURITY ALERTS, SUBSCRIBE TO MY FREE CYBERGUY REPORT NEWSLETTER HERE

We created this article in partnership with Incogni

Copyright 2026 CyberGuy.com. All rights reserved. CyberGuy.com articles and content may contain affiliate links that earn a commission when purchases are made.